THE SUPREME COURT STATES WHAT THE LAW IS ON THE IEEPA AND TARIFFS—IT IS ABOUT THE SEPARATION OF POWERS

INTRODUCTION

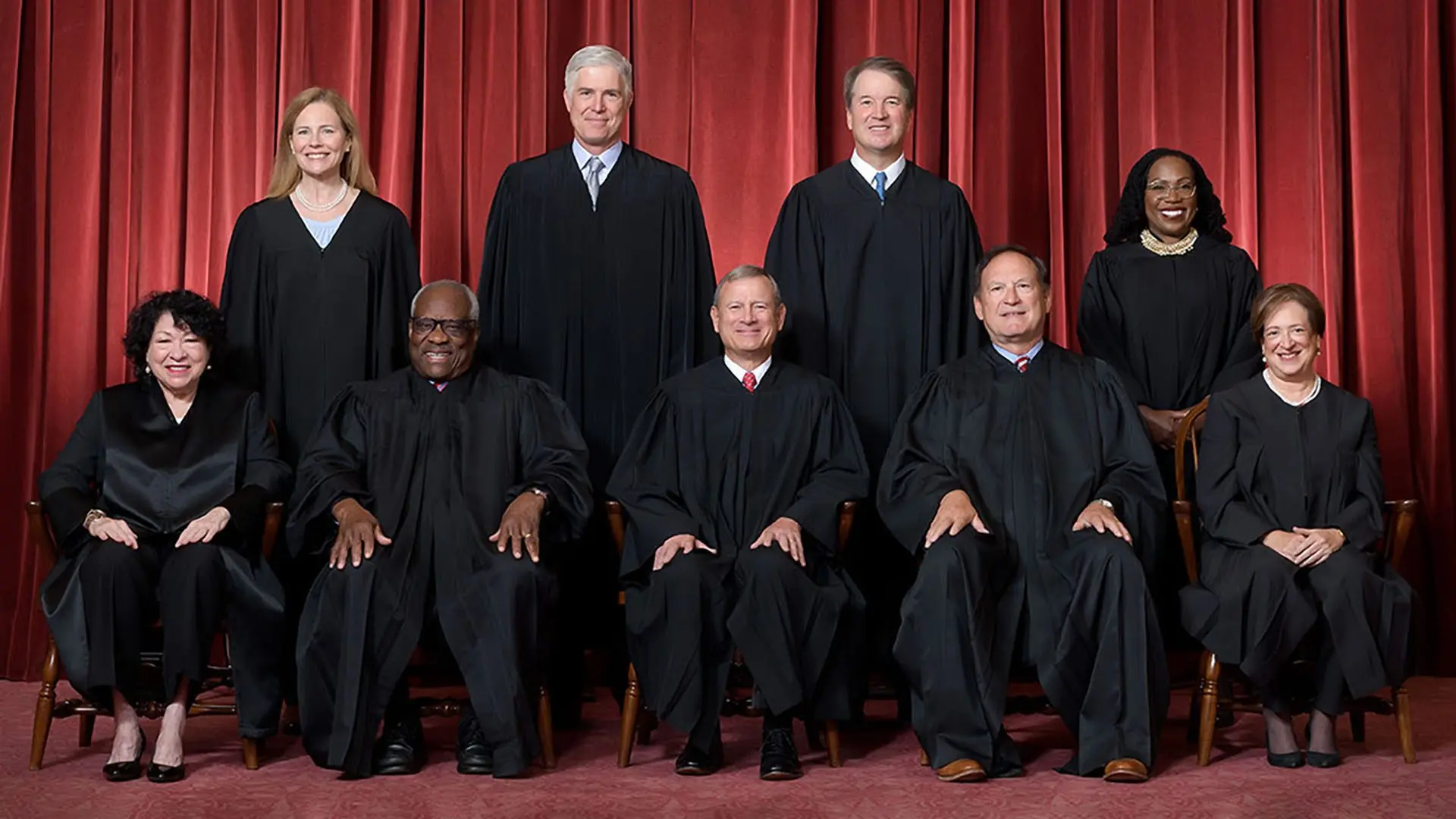

On Friday, the Supreme Court issued a ruling that reinforced the plenary power of Congress set forth in the Article I Vesting Clause to issue and collect taxes and duties. Six of the Justices joined in an opinion that reinforces the major questions doctrine as well as the non-delegation doctrine to ensure that the Executive and Legislative Branches act in accordance with the framework of the separation of powers envisioned by the Framers of the Republic. My goal here is not to weigh in on the wisdom of tariffs as economic policy, political policy, or, indeed, foreign policy. It is to unpack the logic and reasoning of the decision and the dissent through selection of the main points of both, reproduced here in terms easy to comprehend. Distilled in its essence, the following is gleaned from the majority opinion and the dissent.

- The majority essentially held that the Vesting Clause in Article I Section 8 of the Constitution exclusively provides for the tariffs and taxing authority as within the power of Congress.

- That in a situation such as presented here, Congress has not clearly and unambiguously delegated such authority to the Executive—namely, the President.

- The non-delegation doctrine as well as the major questions doctrine prevent a dilution of constitutional powers vested in Congress, absent clear and compelling statutory language and history, and, further, there is no exception regarding the conduct of foreign affairs.

- The dissent of Justices Thomas, Alito, and Kavanaugh sees these doctrines as diluted or not applicable in the foreign affairs context, in which realm they urge this series of Executive Orders resides.

- The dissenting Justices also see that Congress DID delegate this authority by using the broad terms “regulate” and “importation” in the IEEPA, which actions the President was clearly undertaking by identifying national security emergencies sounding in the failure of the targeted nations to stem the flow of fentanyl as well as a rising trade deficit and a crisis in domestic manufacturing.

Justice Gorsuch, in a concurrence, points out the inconsistencies in the liberal wing of the Court’s approach to both major questions and non-delegations’ analyses. He recounts that when the Court struck down Obama’s assault on coal by directing an agency to use an obscure EPA rule and Biden’s loan forgiveness as well as his COVID edicts using OSHA regulations well beyond Congressional delegations of authority, that Justices Kagan and Sotomayor dissented, essentially mocking the major questions doctrine as a convenient invention of the Court and accusing the Court of an “anti-administrative state” stance. Yet, they had no difficulty in applying these principles to strike down tariffs that, if either Biden or Obama had enacted, would have certainly seen them affirm this exercise of executive power. Bravo, Justice Gorsuch.

Although an important strengthening of separation of powers jurisprudence and a consistent application of doctrines that guard against the illusory grant of “emergencies” to achieve political ends—a practice we must be wary of—the case itself is also a tutorial from Justice Kavanaugh (discussed below) that will place the President’s determination to push forward with a tariff agenda on more firm ground. My colleague (and intellectual superior) Ilya Shapiro argues as much in a New York Post piece as well as his outstanding Substack series “Shapiro’s Gavel.” I recommend reading all. Finally, even the most ardent supporter of Trump must be mindful of any President’s declaration of “emergency” and legislation by executive pen. Imagine if a President Ocasio-Cortez declared emergencies that define the socialist agenda, including gun control, and proceeded to act in accordance with that agenda. Biden’s COVID autocracy was condemned across the board by many constitutional scholars for the very same reasons that in large measure guided this majority. Let’s unpack the core reasoning.

JUSTICE ROBERTS WROTE FOR THE MAJORITY, AND THE REASONING FOR THE DECISION IS SET FORTH EARLY IN THE OPINION

“Based on two words separated by 16 others in Section 1702(a)(1)(B) of IEEPA—’regulate’ and ‘importation’—the President asserts the independent power to impose tariffs on imports from any country, of any product, at any rate, for any amount of time. Those words cannot bear such weight.

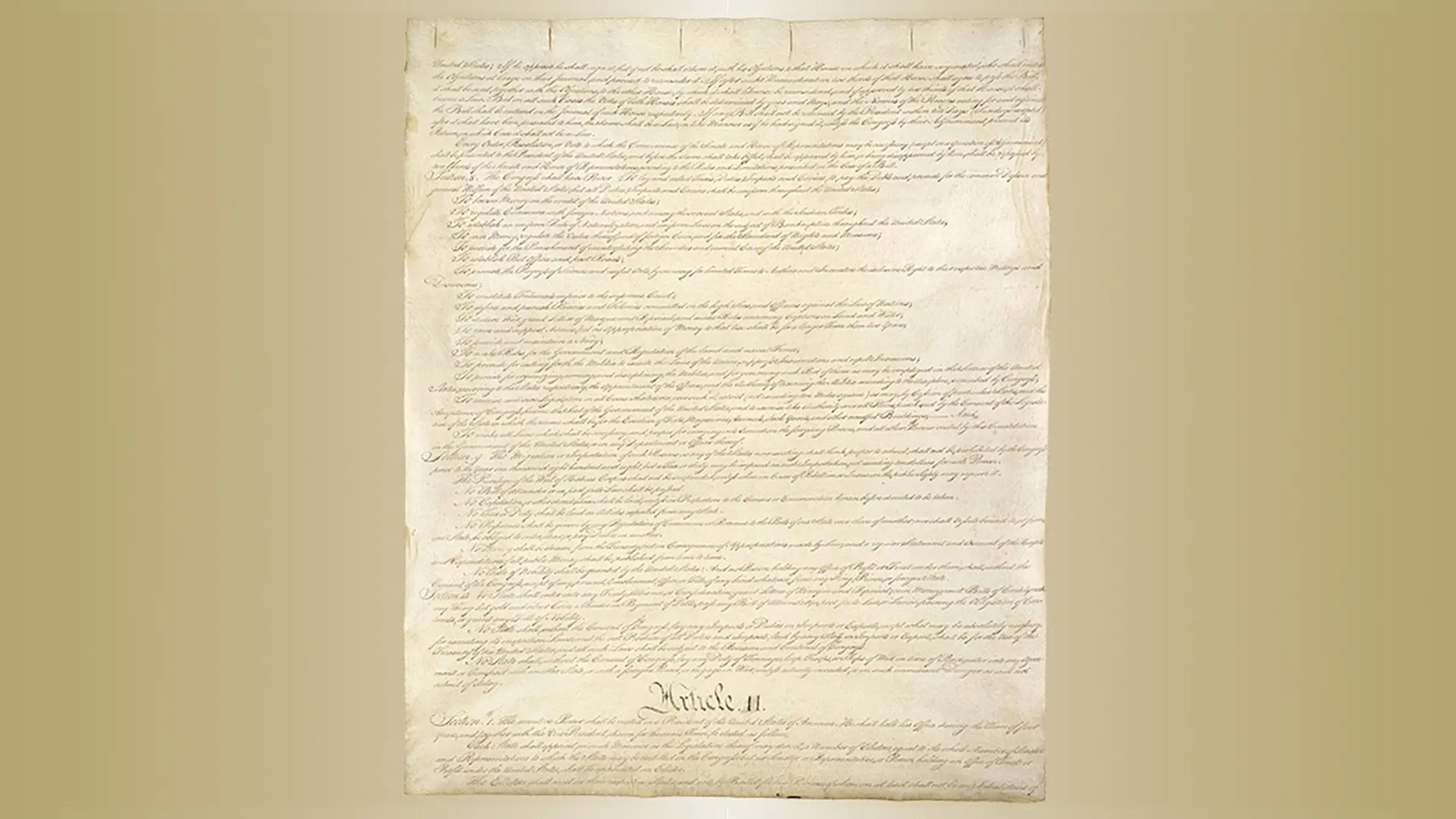

Article I, Section 8, of the Constitution sets forth the powers of the Legislative Branch. The first Clause of that provision specifies that ‘The Congress shall have Power To lay and collect Taxes, Duties, Imposts, and Excises.’ It is no accident that this power appears first. The power to tax was, Alexander Hamilton explained, ‘the most important of the authorities proposed to be conferred upon the Union.’ The Federalist No. 33, pp. 202–203 (C. Rossiter ed. 1961). It is both a ‘power to destroy,’ McCulloch v. Maryland, 4 Wheat. 316, 431 (1819), and a power ‘necessary to the existence and prosperity of a nation’—’the one great power upon which the whole national fabric is based.’ Nicol v. Ames, 173 U. S. 509, 515 (1899).”

THE HISTORY AND POLICIES UNDERLYING CONGRESSIONAL TAXING AUTHORITY ARE SET FORTH

“Recognizing the taxing power’s unique importance and having just fought a revolution motivated in large part by ‘taxation without representation,’ the Framers gave Congress ‘alone . . . access to the pockets of the people.’ The Federalist No. 48, at 310 (J. Madison); see also Declaration of Independence ¶19. They required ‘All Bills for raising Revenue [to] originate in the House of Representatives.’ U.S. Const., Art. I, §7, cl. 1. And in doing so, they ensured that only the House could ‘propose the supplies requisite for the support of government,’ thereby reducing ‘all the overgrown prerogatives of the other branches.’ The Federalist No. 58, at 359 (J. Madison). They did not vest any part of the taxing power in the Executive Branch. See Nicol, 173 U.S., at 515 (‘[T]he whole power of taxation rests with Congress’). The Government thus concedes, as it must, that the President enjoys no inherent authority to impose tariffs during peacetime. And it does not defend the challenged tariffs as an exercise of the President’s warmaking powers.

We have long expressed ‘reluctan[ce] to read into ambiguous statutory text’ extraordinary delegations of Congress’s powers. West Virginia v. EPA, 597 U. S. 697, 723 (2022) (quoting Utility Air Regulatory Group v. EPA, 573 U. S. 302, 324 (2014)). In Biden v. Nebraska, 600 U. S. 477 (2023), for example, we declined to read authorization to ‘waive or modify’ statutory or regulatory provisions applicable to financial assistance programs as a delegation of power to cancel $430 billion in student loan debt. Id., at 494 (quoting 20 U. S. C. §1098bb(a)(1)). In West Virginia v. EPA, we declined to read authorization to determine the ‘best system of emission reduction’ as a delegation of power to force a nationwide transition away from the use of coal. 597 U. S., at 732 (quoting 42 U. S. C. §7411(a)(1)). And in National Federation of Independent Business v. OSHA, 595 U. S. 109 (2022) (per curiam), we declined to read authorization to ensure ‘safe and healthful working conditions’ as a delegation of power to impose a vaccine mandate on 84 million Americans. Id., at 114, 117 (quoting 29 U. S. C. §651(b)); see also, e.g., Alabama Assn. of Realtors v. Department of Health and Human Servs., 594 U. S. 758, 764–765 (2021) (per curiam); King v. Burwell, 576 U. S. 473, 485–486 (2015); Utility Air, 573 U. S., at 324. We have described several of these cases as ‘major questions’ cases. Nebraska, 600 U. S., at 505; West Virginia, 597 U. S., at 732; see also FDA v. Brown & Williamson Tobacco Corp., 529 U. S. 120, 159 (2000) … In each, the Government claimed broad, expansive power on an uncertain statutory basis. And in each, the statutory text might ‘[a]s a matter of definitional possibilities’ have been read to delegate the asserted power. West Virginia, 597 U.S., at 732 (internal quotation marks omitted). But ‘context’ counseled ‘skepticism.’ Id., at 721, 732. That context included not just other language within the statute, but ‘constitutional structure’ and ‘common sense.’ ‘[B]oth separation of powers principles and a practical understanding of legislative intent’ suggested Congress would not have delegated ‘highly consequential power’ through ambiguous language. West Virginia, 597 U.S., at 723–724. These considerations apply with particular force where, as here, the purported delegation involves the core congressional power of the purse. ‘Congress would likely . . . intend[] for itself’ the ‘basic and consequential tradeoffs,’ id., at 730, inherent in uses of this ‘most complete and effectual weapon,’ The Federalist No. 58, at 359. And if Congress were to relinquish that weapon to another branch, a ‘reasonable interpreter’ would expect it to do so ‘clearly.’”

For the purposes of this overview, this sets forth the core reasoning of the majority and establishes that the Court is and will be skeptical of the exercise of power that exceeds constitutional design. The President had declared in his own public statements and through his Solicitor General that this issue was of existential importance to the nation’s economic health and national security. This pronouncement certainly channeled the analysis into the “major questions” line of reasoning.

THE DISSENTING JUSTICES THOMAS, ALITO, AND KAVANAUGH FORCEFULLY REASONED THAT THE STATUTORY LANGUAGE SUPPORTED THE TARIFF EXERCISE OF AUTHORITY AS PROPERLY DELEGATED AND THAT THE FOREIGN AFFAIRS AUTHORITY OF THE EXECUTIVE PRECLUDED THE NON-DELEGATION AND MAJOR QUESTIONS ANALYSIS OF THE MAJORITY

Justice Thomas wrote, in part, as follows, joined by Justice Alito.

“I write separately to explain why the statute at issue here is consistent with the separation of powers as an original matter. The Constitution’s separation of powers forbids Congress from delegating core legislative power to the President. This principle, known as the nondelegation doctrine, is rooted in the Constitution’s Legislative Vesting Clause and Due Process Clause. Art. I, §1; Amdt. 5. Both Clauses forbid Congress from delegating core legislative power, which is the power to make substantive rules setting the conditions for deprivations of life, liberty, or property. Neither Clause prohibits Congress from delegating other kinds of power. Because the Constitution assigns Congress many powers that do not implicate the nondelegation doctrine, Congress may delegate the exercise of many powers to the President. Congress has done so repeatedly since the founding, with this Court’s blessing.

This Court has consistently upheld Congress’s delegation of power over foreign commerce, including the power to impose duties on imports. The Court has long conveyed to Congress that it may ‘invest the President with large discretion in matters arising out of the execution of statutes relating to trade and commerce with other nations.’ Marshall Field & Co. v. Clark, 143 U.S. 649, 691 (1892). Since shortly after the founding, the Court has rejected challenges to delegations of power over foreign commerce.

Congress’s delegation here was constitutional. The statute at issue in these cases, the International Emergency Economic Powers Act, delegates to the President a wide range of powers over foreign commerce. IEEPA gives the President, on conditions satisfied here, the power to ‘regulate’ foreign commerce, including ‘importation’ of foreign property. 50 U.S.C. §1702(a)(1)(B). IEEPA’s delegation of power to impose duties on imports complies with the nondelegation doctrine. Congress delegated to the President a version of the same power that it has delegated to him in many statutes since the early days of the Republic. Congress limited that delegation to foreign commerce. See §1702(a)(1)(B); see also §1701. In delegating the power to impose duties on imports, it gave the President no core legislative power to make substantive rules setting the conditions for deprivations of life, liberty, or property. Its delegation therefore complied with the constitutional separation of powers and is consistent with centuries of practice and precedent.”

JUSTICE KAVANAUGH, WHO HAS A STRONG UNDERSTANDING AND BELIEF IN ARTICLE II PLENARY AUTHORITY, JOINS IN DISSENT AND OFFERS A LIFELINE TO THE EXECUTIVE

“I agree that this case involves an executive action of major economic and political significance—which is typically the trigger for requiring ‘clear congressional authorization.’ But in my respectful view, THE CHIEF JUSTICE’s opinion’s application of the major questions doctrine in this case is incorrect for two alternative and independent reasons. First, the statutory text, history, and precedent constitute ‘clear congressional authorization’ for the President to impose tariffs as a means to ‘regulate . . . importation.’ Second, and in the alternative, the major questions doctrine does not apply in the foreign affairs context. In the foreign affairs realm, courts recognize that Congress often deliberately grants flexibility and discretion to the President to pursue America’s interests. In that context, courts therefore engage in ‘routine’ textualist statutory interpretation—reading the text as written—and do not employ the major questions doctrine as a thumb on the scale against the President…

Presidents imposing tariffs—whether pursuant to inherent wartime authority, pursuant to TWEA and IEEPA’s ‘regulate . . . importation’ language, pursuant to Section 232’s ‘adjust the imports’ text, or pursuant to the many other tariff statutory authorities—is hardly an unusual occurrence in our Nation’s history or in recent times. For example, Presidents George W. Bush, Obama, and Biden all imposed tariffs pursuant to congressional authorization. There is no mismatch between the tariff power and the President’s ‘mission and expertise.’”

ENTER THE LIFELINE AND ROADMAP TO PERHAPS A SOUNDER FOUNDATION IF THE PRESIDENT STAYS THE COURSE WITH NEW ORDERS, WHICH HE HAS ALREADY EXECUTED IN PART

“That said, with respect to tariffs in particular, the Court’s decision might not prevent Presidents from imposing most, if not all, of these same sorts of tariffs under other statutory authorities. For example, Section 122 of the Trade Act of 1974 permits the President to impose a ‘temporary import surcharge’ to ‘deal with large and serious United States balance-of-payments deficits.’ 19 U. S. C. §2132(a). Section 201 of the Trade Act of 1974 provides that, if the International Trade Commission determines an article is being imported in such quantities that it is ‘a substantial cause of serious injury, or the threat thereof, to the domestic industry producing an article like or directly competitive with the imported article,’ the President may take ‘appropriate and feasible action,’ including imposing a ‘duty.’ §§2251(a), 2253(a)(3)(A). Section 301 of the Trade Act of 1974 authorizes the President, through a subordinate officer, to ‘impose duties’ if he determines that ‘an act, policy, or practice of a foreign country’ is ‘unjustifiable’ … ‘or restricts United States commerce.’ §§2411(a)–(c). Section 338 of the Tariff Act of 1930 permits the President to impose tariffs when he finds that ‘any foreign country places any burden or disadvantage upon the commerce of the United States.’ §1338(d). And Section 232 of the Trade Expansion Act of 1962 authorizes the President to, after receiving a report from the Secretary of Commerce, ‘adjust the imports of [an] article and its derivatives so that such imports will not threaten to impair the national security.’ §1862(c)(1)(a). So, the Court’s decision is not likely to greatly restrict Presidential tariff authority going forward. But the Court’s decision is likely to generate other serious practical consequences in the near term. One issue will be refunds. Refunds of billions of dollars would have significant consequences for the U.S. Treasury. The Court says nothing today about whether, and if so how, the Government should go about returning the billions of dollars that it has collected from importers. But that process is likely to be a ‘mess,’ as was acknowledged at oral argument… A second issue is the decision’s effect on the current trade deals. Because IEEPA tariffs have helped facilitate trade deals worth trillions of dollars—including with foreign nations from China to the United Kingdom to Japan, the Court’s decision could generate uncertainty regarding various trade agreements. That process, too, could be difficult… The tariffs at issue here may or may not be wise policy. But as a matter of text, history, and precedent, they are clearly lawful.”

CONCLUSION

The political impact of the decision is clear. Hypocrites on the left who applauded Obama’s and Biden’s power grabs will frame this as poisonous chaos going into the midterms and evidence of Trump’s “autocracy.” The President, right or wrong, is committed to the role of tariffs as a revenue-generating measure, an incentive for foreign manufacturers to build in the United States, and, finally, leverage to enter more advantageous trade deals. Many such deals have already been forged. One would hope their terms include boilerplate provisions to defend against any such ruling as issued by the Supreme Court, including a waiver of any refunds as a quid pro quo for tariff relief and reduction. The Treasury Secretary and the Secretary of Commerce are doubtless currently working to put into place a defensive posture to protect what has been collected and to make proclamations that would power future tariffs under the different provisions cited by Justice Kavanaugh. Unfortunately, current statistics still point to a static and even an increased trade deficit given an increase in imports, notwithstanding the tariffs. Some of our trading partners have been driven into the arms of China or Europe. Billions in revenue remain in limbo. On the other hand, inflation is stable and the economy is strong and growing. This chaos, however, regarding the status of revenue collected, will remain well past the midterms as the administration will resist demands for clawback. Promises of checks to the American public are on hold. Additional leverage for future trade deals may have been presented.

In the end, I will always resist the erosion of the separation of powers through the declaration of “emergencies” that are not true emergencies. In such an environment the Republic will dissolve.

Mike Imprevento

February 23rd, 2026